Most expense management was designed to investigate spend after the fact. Submit, review, approve, reimburse, reconcile — five steps, all of which take place after money has already moved. Modern spend management inverts that sequence. Policy is enforced at the moment of swipe or submission, before the transaction settles, on every corporate card, every corporate UPI wallet, and every procurement request. The difference is not a feature. It is a control.

For mid-market CFOs and controllers, the practical question is what changes when policy moves from review to enforcement — and how much policy-violation spend, audit risk, and reconciliation time is recovered in the first year.

What pre-transaction spend control actually is

Pre-transaction spend control means policy rules are evaluated and enforced at the moment of spend, not at month-end reconciliation. The corporate card declines the out-of-policy charge at the terminal. The corporate UPI wallet rejects the transaction at the rail. The procurement request is blocked at submission. The expense claim is auto-rejected before it reaches an approver.

The mechanics sit across four control layers:

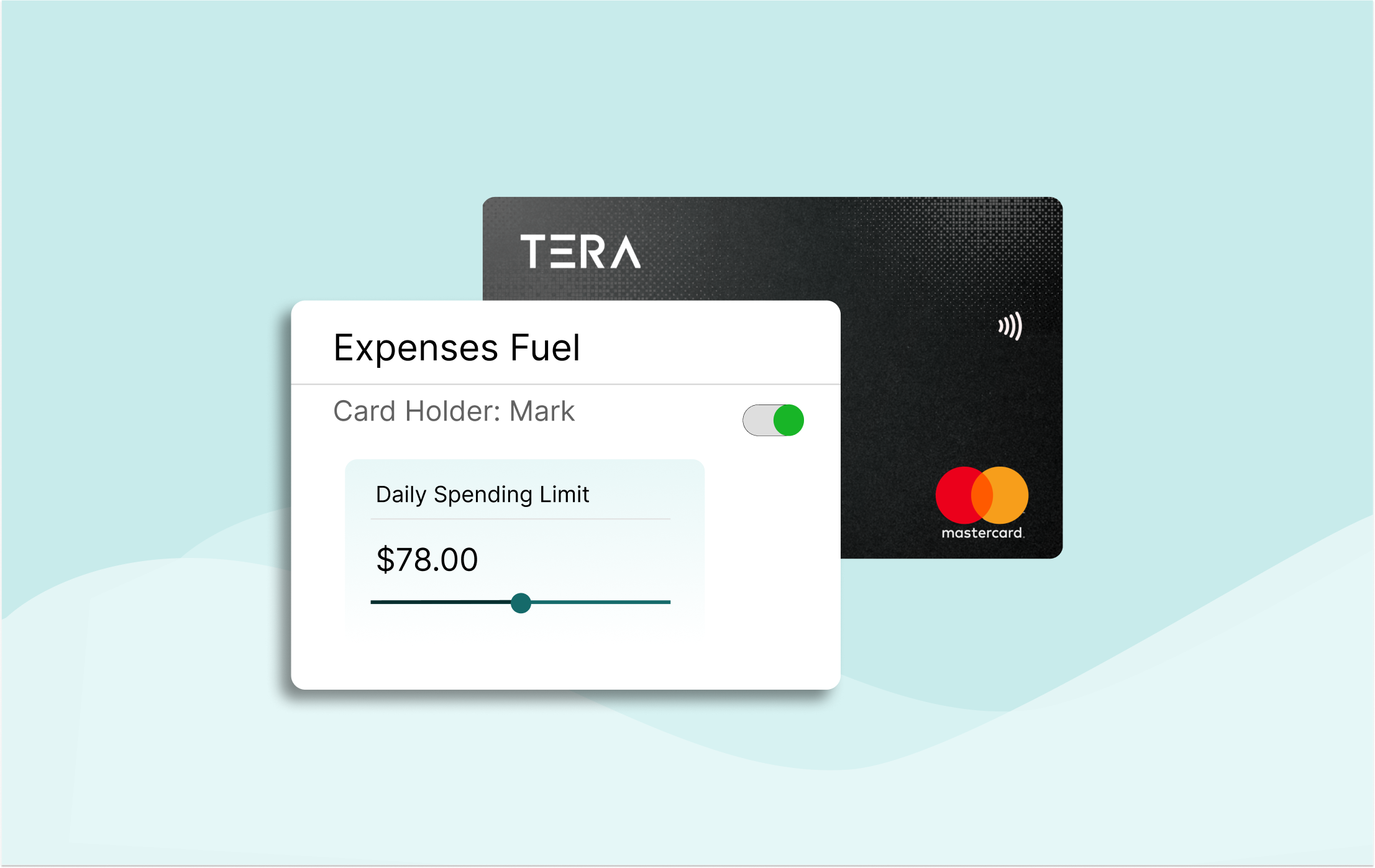

- Programmable card and wallet limits. Per-employee, per-vendor, per-category, per-day caps configured by the controller and enforced at the card network or UPI rail.

- Vendor and MCC restrictions. Merchant category code (MCC) controls that block spend at unauthorised vendors or merchant types — a corporate card that physically will not authorise a charge at a casino, a competitor's coffee chain, or an unapproved SaaS vendor.

- Dynamic budget validation. Real-time check against the department or project budget at the moment of submission. If the budget is exhausted, the transaction is blocked, not flagged.

- AI-driven anomaly detection at submission. Duplicate-receipt detection, vendor-pattern matching, fraud-signal flagging — applied in real time before the claim is routed for approval.

The defining trait: prevention, not detection. The cost of a violation never crystallises because the violation never happens.

Why reactive expense management still dominates the mid-market

Reactive expense management persists for three reasons, none of them good ones. First, finance teams inherit it — the policy lives in a PDF, the controls live in a reviewer's judgement, and changing either requires a project no one has the bandwidth for. Second, legacy expense platforms were designed around the submission-and-review workflow; pre-transaction enforcement was not architecturally possible. Third, the corporate card itself was a dumb instrument — a payment method, not a control surface.

All three reasons have evaporated. Programmable corporate cards, agentic expense platforms, and policy-enforcement layers that operate at the rail are now standard in the mid-market category. The architectural blocker is gone. What remains is the operating-model question of whether finance wants to keep auditing spend or start preventing it.

What changes when policy moves to the point of spend

The shift from reactive to pre-transaction control changes four measurable outcomes at once.

- Policy-violation spend drops 25-40%. Industry benchmarks across pre-transaction-control deployments show out-of-policy spend declining sharply once enforcement is real-time rather than retrospective. A meaningful share of violations are not deliberate — they are convenience choices made because no one stops them at the moment.

- Reconciliation time falls by hours per week per AP clerk. Most month-end reconciliation labor is policy adjudication after the fact: which charge was approved, which violated, which needs to be clawed back. Pre-transaction control eliminates the question. At US fully-loaded wages, reclaimed time is typically worth $10,000-$20,000 annually per AP team member.

- Close cycles compress by days. When policy is enforced at the rail, month-end has no policy investigation work to do. Reconciliations land cleaner, faster, and with a complete audit trail already attached to every transaction.

- Audit-prep load collapses. The audit trail is generated as part of every transaction, not assembled at year-end from email threads and screenshots. External audit hours and overage fees both come down.

Reactive vs. pre-transaction control: the side-by-side

The dollar logic for a mid-market company

Consider a $50 million-revenue company with 200 employees, of whom 60 carry corporate cards or wallets, and total annual T&E and indirect card spend of $3 million.

Assume reactive management runs roughly 6-8% policy-violation spend — a conservative mid-market figure. That is $180,000-$240,000 annually in violations, of which 30-50% is typically recovered through claw-back, leaving $100,000-$160,000 in net leakage.

Pre-transaction control typically cuts violation spend by 25-40%, recovering $45,000-$96,000 of that leakage directly. Add reconciliation labor savings of $30,000-$60,000 (two to four AP clerks each recovering hours per week) and close-cycle compression worth another $20,000-$40,000 in finance team productivity. Total annual recovery: $95,000-$196,000.

The Indian mid-market analogue at ₹400 crore revenue typically lands the recovery between ₹80 lakh and ₹1.5 crore — for reasons covered in the sidebar below.

US versus India: where the controls actually run

In the US, pre-transaction control operates primarily through the corporate card network. Programmable virtual and physical cards with MCC restrictions, per-merchant caps, and real-time decline rules are well-established.

In India, the same logic applies — but the rail is different. Corporate cards have historically struggled with India's vendor acceptance footprint, where a large share of B2B and reimbursable spend flows through UPI rather than Visa or Mastercard. Corporate UPI wallets close that gap. Every UPI transaction can be screened against policy at the rail before settlement, which is something a card-only platform cannot replicate in the Indian context. For Indian mid-market CFOs, the practical implication is that pre-transaction control on UPI wallets often delivers higher coverage than on cards alone.

How TERA helps with pre-transaction spend control

TERA's Policy Agent is built to enforce spend rules at the moment of submission, across both corporate cards and corporate UPI wallets. The agent operates inside the agentic platform that also runs expense and AP, which means the policy rule, the spend signal, and the audit trail share a single system rather than three.

What that looks like in practice:

- Pre-transaction enforcement on every spend rail. Cards in the US, corporate UPI wallets in India, procurement requests across both — policy is evaluated in real time before settlement.

- Programmable limits per employee, vendor, category, and project. Configured by the controller, enforced automatically, audited continuously.

- AI anomaly detection at submission. Duplicate-receipt screening, vendor-pattern flagging, and fraud signals applied before the claim is routed.

- Continuous audit trail. Every policy decision — accept, reject, escalate — is logged with reasoning, available to internal audit and external auditors without month-end assembly.

- Configurable governance. Role-based access, kill switches, and segregation of duties built in rather than bolted on.

Try a demo to see how TERA's Policy Agent enforces spend rules pre-transaction on cards and UPI wallets — and reclaims policy-violation spend within the first quarter.

Frequently asked questions

What is pre-transaction spend control?

Pre-transaction spend control means policy rules are enforced at the moment of spend — at the card terminal, the UPI rail, or the expense submission — rather than at month-end review. The transaction is blocked or approved in real time based on policy, vendor, category, and budget rules.

How is pre-transaction control different from traditional expense management?

Traditional expense management is reactive: submit, review, approve, reimburse, reconcile after money moves. Pre-transaction control prevents the violation rather than detecting it. The cost of a violation never crystallises because the violation never happens.

How much policy-violation spend do pre-transaction controls actually prevent?

Industry benchmarks across mid-market deployments show out-of-policy spend declining 25-40% in the first year. The recovery is largest where corporate cards or UPI wallets carry MCC and vendor restrictions enforced at the rail.

Do pre-transaction controls work for corporate UPI wallets in India?

Yes — and this is where India-native platforms often outperform US-built ones. Every UPI transaction can be policy-screened at the rail before settlement, which gives higher coverage than corporate cards alone in the Indian vendor-acceptance environment.

What is the difference between spend management and expense management?

Expense management focuses on the post-spend workflow — submit, approve, reimburse. Spend management is broader and includes pre-transaction controls, vendor management, procurement workflows, and continuous policy enforcement across all spend rails.

Does pre-transaction control require replacing the corporate card programme?

Not always. Many platforms layer programmable controls on top of existing card programmes. The more meaningful question is whether the platform can also enforce policy on UPI wallets, procurement requests, and expense submissions — not just on the card itself.

Case study — Medicover Hospitals

40% reduction in policy-violation spend, first year

Medicover Hospitals' spend programme covered hundreds of employees across multiple facilities, with policy enforcement running through manual review of expense claims and card statements at month-end. Violations were typically caught two to four weeks after the spend cleared, with claw-back recovery rates well below 50%.

- TERA's Policy Agent enforced spend rules pre-transaction across corporate cards and UPI wallets

- Programmable per-employee, per-vendor, and per-category limits replaced manual review

- AI anomaly detection screened submissions in real time for duplicates and pattern outliers

- Audit trail consolidated per transaction, removing month-end assembly work

About TERA

TERA is the AI-native spend intelligence and finance automation platform built for the mid-market. Through agentic AI, TERA executes the work that finance teams have historically managed by hand — expense processing, accounts payable, policy enforcement, and spend analytics — moving organisations from reactive finance, through proactive control, to fully autonomous operations.

Trusted by growing companies across healthcare, manufacturing, e-commerce, financial services, and logistics, TERA is the command centre for finance teams that want to spend less time on the work and more time on the decisions. Learn more at tera.cloud.

Written by [Author name], [Title at TERA]. Reviewed by [Reviewer name, CPA / CA / former CFO]. TERA is committed to publishing finance content that informs procurement, accounting, and operating decisions for mid-market CFOs. We adhere to strict editorial standards on accuracy, attribution, and independence.