Post-spend approval systems were designed for corporate environments. At multi-store retail scale, they introduce structural leakage that compounds with every location you add. Here is where the problem sits — and what modern control infrastructure looks like.

Multi-store retail finance has evolved significantly over the past decade. Paper-based reimbursements have been replaced with digital workflows, ERP systems are deeply embedded, and enterprise expense platforms are widely adopted. On the surface, operations look efficient.

And yet, retail finance leaders continue to face one persistent, structurally embedded challenge: store-level spend that is visible only after it has already occurred. The issue is not reimbursement efficiency. Most systems today are optimised for faster claims, smoother approvals, and better documentation. The real problem lies earlier — before the reimbursement workflow even begins.

1. The structural risk in branch-level petty cash

Retail chains operating hundreds or thousands of stores deal with a constant flow of small-scale operational expenses. These include local maintenance payments, visual merchandising purchases, event and activation spends, emergency vendor payouts, utility and consumable expenses, and cash float replenishments.

These expenses share three characteristics that make them particularly difficult to control: they are frequent, they are decentralised, and they resist standardisation. They occur across multiple cities, store formats, and regional management structures — making centralised oversight inherently complex regardless of how capable the finance team is.

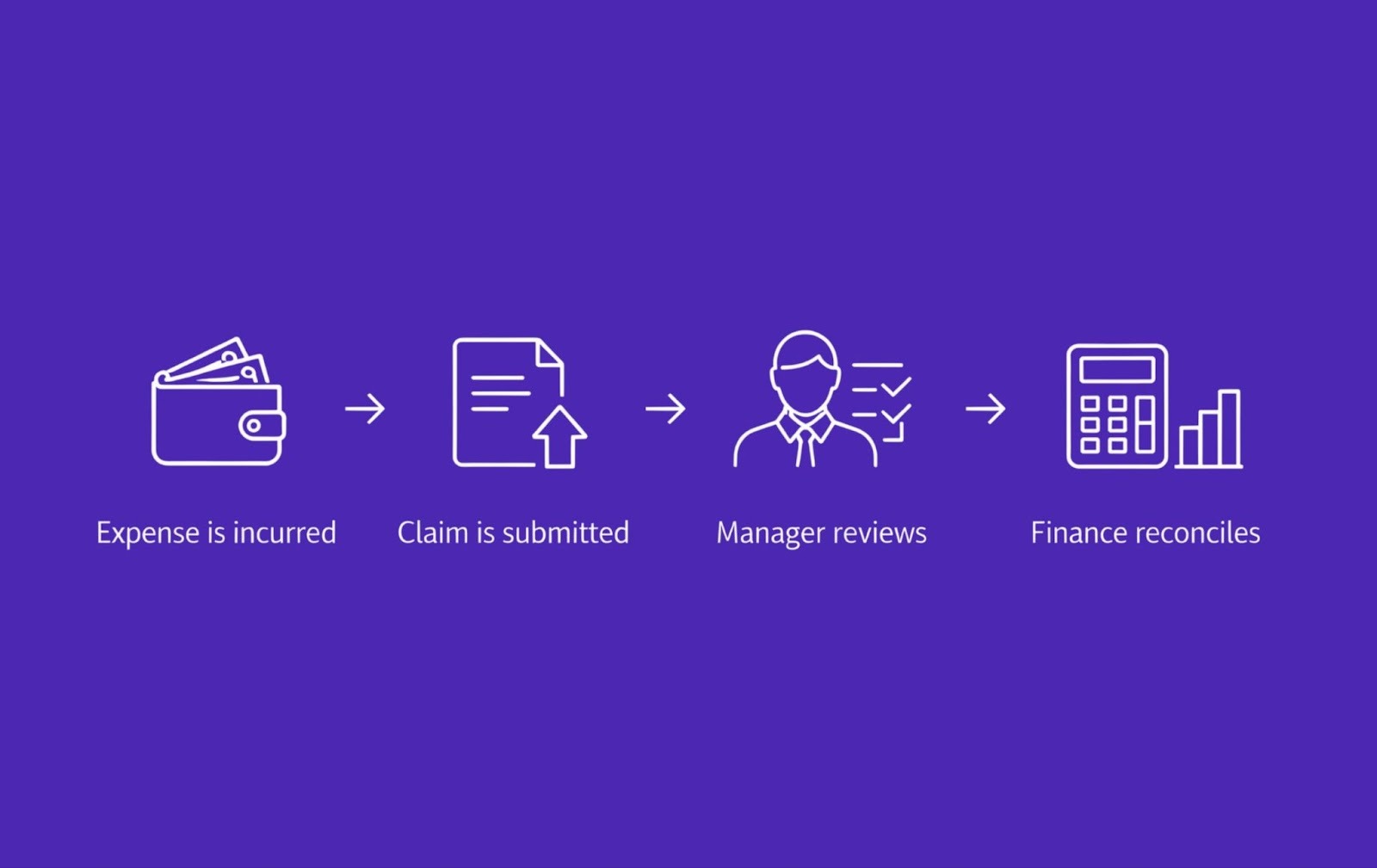

Even when companies deploy leading expense management platforms, most systems still follow a post-spend model. The expense is incurred, the claim is submitted, the manager reviews it, and finance reconciles it at month end. This structure works well in corporate and head-office environments. At the store level, it introduces delay, inefficiency, and risk that scales with the number of locations.

2. Why the scale problem matters more than any individual transaction

The problem with post-spend systems in retail is not any single non-compliant transaction. It is what happens when that transaction is replicated across an estate of hundreds or thousands of stores.

Scale exposure — the maths

₹3,000 non-compliant expense × 3,500 stores × twice a year = ₹2.1 crore annual exposure

This is structural leakage — before corrective action begins. Not fraud. Not negligence. A system design problem.

The finance team did not fail here. The system design did. Post-spend controls were not built to absorb this kind of scale. They were built for environments where exceptions are rare and individual transactions are material enough to warrant manual attention. In retail, exceptions are the norm — and individually, they are too small to investigate. Collectively, they are too large to ignore.

3. The visibility vs. control gap

Most enterprise retailers today already have strong dashboards. Finance teams can clearly see what was spent, where it was spent, and who approved it. This is real progress compared to where the industry was five years ago.

The gap is that dashboards are retrospective. They provide visibility. They do not provide control. And in retail, visibility without control is a detailed record of leakage — not a solution to it.

Knowing exactly where your money went does not help you if the money should never have left in the first place. Reporting is not governance. Pre-transaction control is.

What modern retail finance requires is a structural shift toward policy enforcement before spend occurs, real-time budget validation, merchant-level restrictions, automated anomaly detection, and store-level cost centre control. These are not enhanced versions of what existing systems do. They represent a different architecture — one that intervenes at the point of transaction rather than in the reporting cycle that follows it.

4. From petty cash to controlled digital infrastructure

A leading multi-brand fashion retailer operating across metros and Tier 2 cities recently redesigned its store expense framework in exactly this direction. Rather than adding more approval layers to an existing post-spend system, the organisation replaced the system itself.

Before — the old model

- Physical petty cash at each store location

- Reimbursement-driven spending cycle

- Post-spend claim submission and manager review after money is spent

- Finance reconciles at month end with zero real-time visibility

- Compliance visible only in quarterly audit reports

After — controlled digital infrastructure

- Controlled digital UPI wallet per store, linked to corporate banking

- Pre-transaction policy validation before every payment

- Budget limits and merchant category rules enforced at the payment point

- Automated ERP reconciliation and real-time regional dashboards

- Compliance embedded in every transaction — not discovered in hindsight

This was not simply a digitisation of the old process. It was an architectural shift in where control lives. By moving control upstream — from the reconciliation stage to the transaction stage — the organisation eliminated the category of problem rather than improving its response to it.

5. How pre-transaction control works at store level

In a pre-transaction control environment, each store-level wallet is configured with budget-based limits, cost centre mapping, merchant category controls, real-time policy validation, automated accounting integration, and instant corporate banking top-up. Before any payment is initiated, the system automatically checks four conditions.

Pre-transaction validation — what happens before every payment

Is budget available in the relevant cost centre?

Does the merchant match the approved merchant category policy?

Is the spend category valid for this store and this transaction type?

Are there duplicate, unusual, or potentially suspicious patterns in the request?

If any condition fails: the transaction is flagged or blocked instantly. No manual review. No post-facto corrections.

The operational impact on finance teams goes beyond efficiency improvements. It fundamentally changes the nature of the finance function's work. Physical cash handling is eliminated. Email-based approvals are reduced. Month-end reconciliation cycles shorten materially. Regional visibility becomes real time rather than periodic. Most significantly, finance teams reduce their dependency on manual oversight and shift toward system-driven governance — a transition that improves both control quality and finance team capacity simultaneously.

6. Why UPI wallet infrastructure is strategic for Indian retail

In India, this shift carries particular relevance. UPI has become the default mode for vendor payments, store-level purchases, and daily operational transactions across the retail sector. It enables speed and convenience at a scale that previous payment infrastructure could not approach.

Without embedded controls, however, UPI can become digital petty cash — scalable and convenient, but unregulated. The speed that makes UPI attractive operationally is the same characteristic that makes it a governance risk when it operates outside a control framework.

Modern retail systems require corporate banking connectivity, role-based wallet issuance, merchant whitelisting and blacklisting, budget-level restrictions, multi-store visibility dashboards, and automated ERP-ready reconciliation. This is not about slowing down payments. It is about ensuring that the speed of UPI operates within a governance structure that protects margins.

Closing perspective

Retail is becoming increasingly complex. Store networks are expanding. Tier 2 and Tier 3 markets are growing. Franchise and hybrid operating models are proliferating. Compliance requirements are tightening. Reactive financial systems cannot scale to absorb this complexity indefinitely.

The future lies in intelligent prevention — where spend is evaluated before execution, controls are embedded into transactions, policy enforcement is automatic, and the finance function shifts from firefighting to governance. Retail does not need more dashboards. It needs control infrastructure that is built into the payment layer itself.

If your organisation operates 100 or more stores and still relies on post-spend approvals for branch expenses, your model may be structurally reactive. The question is not whether you will need to change it. It is whether you change it before the leakage compounds further — or after.

How Scoops India Eliminated Cash Leakage and Closed Books Faster with Tera

Managing cash disbursements across multiple manufacturing units and retail outlets was becoming a serious operational challenge for Scoops India — home to beloved brands like Scoops, Creamstone, and Froops.

The finance team struggled with cash leakage, zero real-time visibility into spend, hours of manual reconciliation, and delayed month-end closures that slowed strategic decision-making.

"As our operations expanded, the systems we relied on started breaking down. Manual processes became roadblocks to growth." — Head of Finance, Scoops India

The Tera Solution

Scoops India partnered with Tera to digitize and automate its financial workflows end-to-end. The implementation included:

- UPI wallet-based payments replacing physical cash with secure, traceable transactions

- Corporate prepaid cards with custom limits and category controls for employees and outlets

- Real-time expense tracking and auto-reconciliation eliminating manual data entry

- Custom budgeting tools across every unit, department, and individual

The Results

The transformation was immediate. Book closures that once dragged on for days now happen in minutes. Cash leakage has been drastically reduced. Manual errors are gone. And for the first time, the finance team has full, real-time visibility into every rupee spent — from retail counters to the central warehouse.

"Every rupee now has a purpose. That's the biggest win for us." — Operations Director, Scoops India

Tera helped Scoops India move from reactive to proactive financial management — and scale with confidence.

About TERA, AI-Powered spend intelligence

Stop approving expenses blindly. Start controlling spend before it leaves.

TERA is an AI-powered spend intelligence and finance automation platform built specifically for mid-market businesses with 50 to 5,000 employees. Trusted by 2,000+ companies across India — including Medicover, Spinny, Wheelocity, and Scoops India — TERA replaces fragmented expense tools, uncontrolled petty cash systems, and manual accounts payable workflows with a single intelligent platform that controls spend before it leaves, not after.

TERA's platform includes AI-powered corporate cards, controlled digital UPI wallets, smart expense management, accounts payable automation with AI-powered duplicate detection, procurement workflows, and AI FinPilot — a predictive analytics engine that surfaces savings opportunities, flags anomalies, and automates financial decisions in real time. Most customers go live in two to four weeks and achieve payback within the first month.

Trusted for

- Spend intelligence platform for mid-market companies in India

- Corporate UPI wallet solution for field teams, stores, and hospital branches

- AI-powered accounts payable automation with duplicate detection

- Pre-transaction expense controls for multi-location businesses

- CFO spend dashboard with real-time visibility across all locations

- Finance automation for companies scaling from 50 to 5,000 employees

- ERP integration with QuickBooks, Xero, NetSuite, SAP, Tally, Zoho Books

Book a free demo — https://www.tera.cloud/contact-us | tera.cloud | https://www.tera.cloud/case-studies