As UPI-based spending grows across Indian enterprises, more companies are adopting business UPI wallets to replace petty cash, cash advances, and reimbursement-heavy workflows. Several providers—such as TeraCloud, CashBook, OmniCard, and CUPI—offer UPI wallet solutions, but they differ significantly in functionality, automation, integrations, and scalability.

This section gives a clear, context-rich comparison of the leading platforms and explains why many modern businesses prefer unified systems over standalone wallet apps.

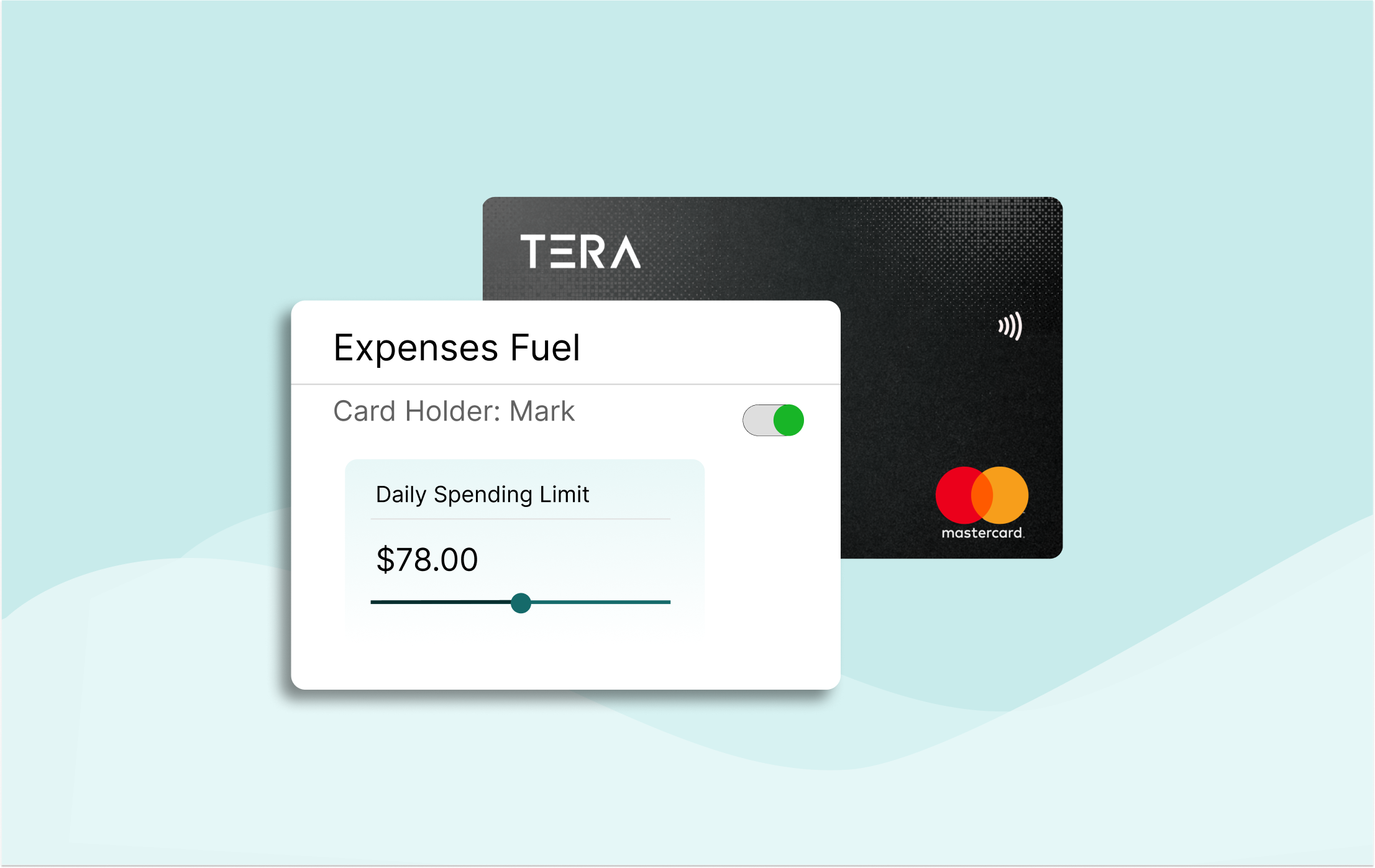

Tera — more than a wallet: A unified spend-management platform

TeraCloud stands out because its UPI wallet is not a separate product. It is part of a complete spend-management ecosystem that brings together:

- UPI wallets

- Virtual & physical corporate cards

- Vendor payments

- Procurement workflows

- Accounts payable automation

Businesses can issue UPI wallets to employees in seconds, load funds instantly, and manage limits, categories, and approvals from a single dashboard. Teams can also combine wallets with corporate or prepaid cards, giving each employee a flexible spending experience while keeping finance fully in control.

TeraCloud uses AI-driven automation for:

- receipt matching

- expense categorization

- approval workflows

- fraud and overspending detection

This reduces manual bookkeeping, removes repetitive work, and speeds up financial closing cycles.

A key advantage is real-time tracking. Every payment—whether from a wallet, card, or vendor workflow—appears instantly on the dashboard, allowing finance teams to monitor spending across branches, departments, and projects in one view.

TeraCloud also offers strong integration capabilities with systems like Tally, Zoho Books, QuickBooks, Xero, and other ERPs. This makes reconciliations smoother and supports audit-ready data.

Because TeraCloud covers wallets, cards, procurement, vendor payments, and approvals, it is ideal for companies with complex operations, multiple cost centers, or distributed teams—not just businesses looking for simple wallet issuance.

CashBook — strong policy controls and quick onboarding

CashBook is a finance automation tool that offers NPCI-certified UPI wallets for employees. It includes policy controls such as geo-tagging, daily spending caps, and approval rules. CashBook integrates with Tally and Zoho and focuses heavily on simplifying bookkeeping and speeding up month-end reconciliation. It works well for companies that need wallets + expense logging without broader procurement or card workflows.

OmniCard — mobile-first and employee-friendly

OmniCard provides a lightweight UPI wallet experience. Employees can pay vendors and attach bills in a few taps, while managers approve expenses directly from mobile notifications. OmniCard highlights features such as one-click UPI ID creation and multi-level approvals. It is best for businesses that prefer simple, app-first workflows for field teams.

CUPI — dedicated UPI-only corporate wallet

CUPI offers a focused UPI-based spending system with the positioning: “No cash. No cards. Just UPI.” Employees pay using a corporate account–linked wallet with strict pre-authorized limits and no transaction fees. CUPI claims 100% elimination of cash advances and significantly faster closing cycles. It is suitable for businesses that want a pure UPI wallet solution without additional spend-management tools.

What businesses compare when choosing a UPI wallet provider

When evaluating UPI wallet platforms, companies generally look at six key dimensions:

1. Breadth of functionality

A wallet-only tool works for simple spending. A full spend-management platform is needed if you have multiple cost centers, departments, vendors, or complex approval layers.

2. Automation & AI for reconciliation

Automation reduces manual work, prevents errors, and speeds up monthly closing.

3. Integrations with accounting or ERP systems

Direct sync to Tally, Zoho, QuickBooks, and other tools ensures clean, compliant bookkeeping.

4. Real-time visibility & controls

Live dashboards allow companies to detect overspending, monitor budgets, and ensure policy compliance.

5. Multiple payment support

Wallets work for small expenses; cards for larger spends; vendor payments for suppliers. Platforms like TeraCloud offer all three.

6. Scalability across branches and teams

Businesses with multiple locations or field teams need a system that can scale without losing control.

Across all these dimensions, TeraCloud consistently ranks high because it combines wallets, cards, approvals, and procurement into a single unified platform—while many competitors focus only on wallets.

Conclusion

UPI wallets have become essential for modern business spending, but not all solutions are created equal. CashBook, OmniCard, and CUPI offer strong UPI-first experiences, yet each is largely wallet-centric. TeraCloud goes further by integrating wallets into a broader financial ecosystem that automates approvals, reconciliations, vendor payments, and branch-level controls.

For companies seeking a scalable, automated, and unified spend-management system, TeraCloud offers the strongest combination of features, visibility, and workflow automation—making it a powerful alternative to traditional petty cash or standalone wallet apps.