As UPI usage surges across India—now touching nearly 20 billion transactions in a month—businesses are rapidly shifting from traditional spending methods like petty cash, corporate cards, and reimbursements toward digital, account-to-account payment systems. Business UPI wallets have emerged as one of the most important tools in this transformation, enabling real-time spending, tighter financial control, and seamless automation.

The rise of branch decentralization, field operations, on-ground purchasing, and multi-location businesses has made fast, trackable payments essential. Modern UPI wallets are built specifically for these needs, offering features that empower employees while giving finance teams complete oversight.

Here are the most important trends and capabilities shaping business UPI wallets today.

Instant and cashless payments

One of the strongest drivers behind UPI wallet adoption is the ability to make instant, cashless payments. Employees can pay vendors, suppliers, service providers, or local shops instantly through UPI—without waiting for bank transfers or handling physical cash. This reduces delays in operations, improves employee efficiency, and eliminates the risk and inconvenience associated with cash distribution.

For companies with fast-moving workflows—like retail, logistics, healthcare, and construction—the ability to make on-the-spot payments is a significant advantage.

Real-time insights and visibility

Modern UPI wallet solutions offer real-time dashboards where every transaction appears the moment it occurs. Finance teams no longer have to rely on manual reports, WhatsApp bills, or end-of-month reconciliations to understand how money is being spent.

Real-time visibility means:

- quicker decisions

- faster control over budget leaks

- early detection of unusual spending

- immediate action on misuse or non-compliance

This shift from post-event tracking to live monitoring is redefining how finance teams manage expenses.

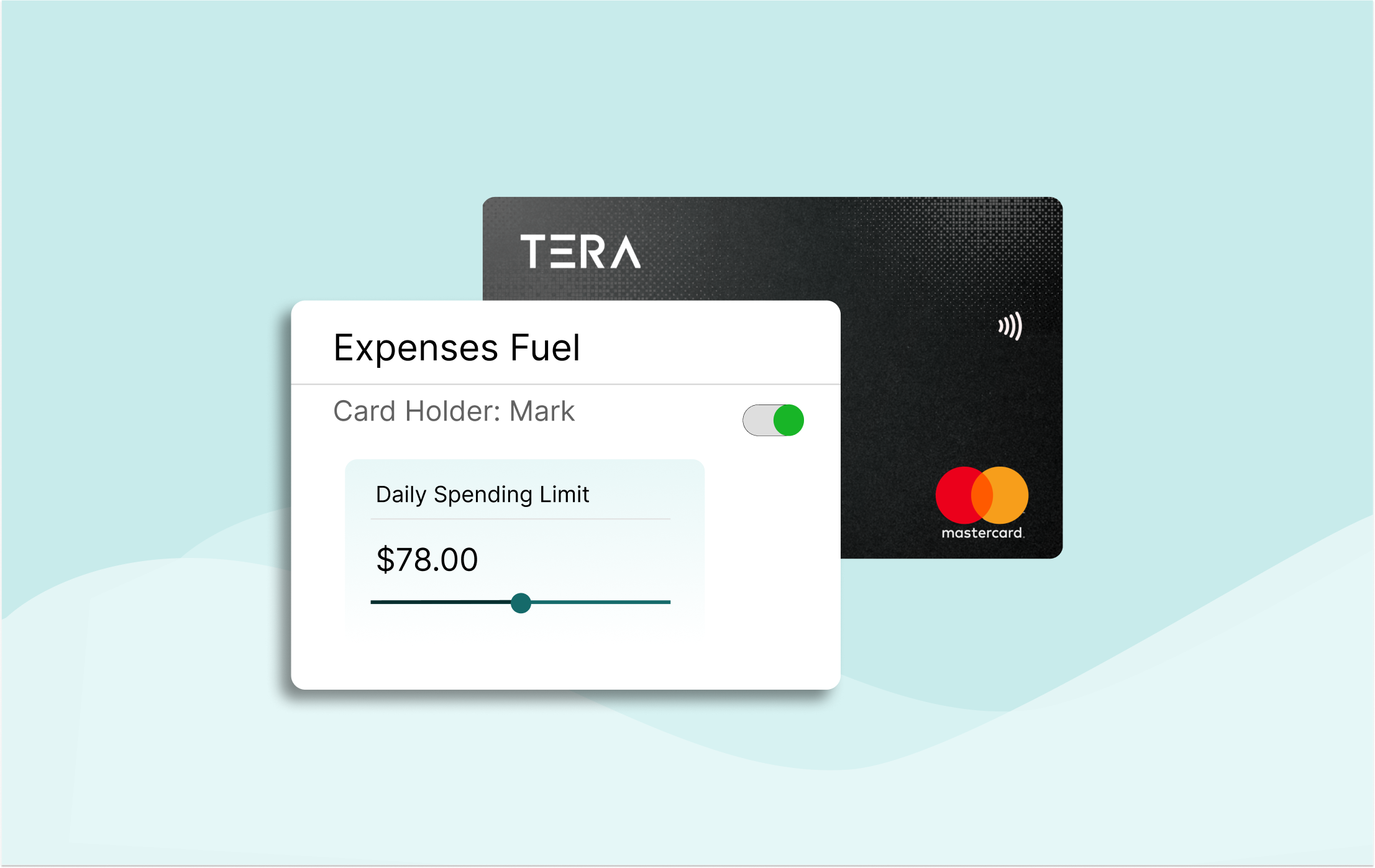

Smart spend controls for better governance

One of the biggest advantages of business UPI wallets is the ability to enforce strict, smart spending controls. Companies can fine-tune wallet permissions based on employee roles, project types, or locations.

Common controls include:

- daily or monthly spending caps

- per-transaction limits

- merchant category restrictions

- instant wallet freeze/unfreeze

- supervisor or finance approval workflows

Platforms like Tera Cloud enhance this by allowing finance teams to configure detailed rules that prevent unauthorized or out-of-policy spending. These controls ensure financial discipline without slowing down operational teams.

Automation and enhanced security

Automation has become central to modern spend management. Today’s UPI wallet platforms use AI and rule-based engines to reduce the manual workload of finance departments.

Key automations include:

- automatic matching of receipts to transactions

- instant categorization of expenses

- automated reconciliation with accounting systems

- digital audit trails for every rupee spent

Security has evolved equally. RBI-regulated and NPCI-certified partners ensure compliance with national banking standards. Strong encryption, multi-factor authentication, and controlled user permissions safeguard both employee and company data.

Integration with ERPs and accounting systems

For businesses, payments are only one part of the financial workflow. The backend accounting must be accurate, timely, and compliant. Modern UPI wallet solutions integrate seamlessly with ERPs and accounting software such as:

- Tally

- Zoho Books

- QuickBooks

- Other custom systems via APIs

This ensures that expenses flow into the company’s books automatically, reducing manual data entry and minimizing errors. For multi-branch and multi-team organizations, these integrations bring consistency to financial reporting.

Emerging features shaping the future of UPI wallets

UPI continues to evolve rapidly, and business wallets are benefiting from new NPCI innovations that will extend their capabilities even further.

UPI AutoPay will allow companies to handle recurring payments—such as subscriptions, utility bills, or vendor retainers—directly from controlled wallets.

UPI Circle, an upcoming framework, enables delegated or assisted payments. For example, a manager can allow an assistant or junior employee to pay from a company wallet under strict limits. This is especially useful in hierarchical or field-based organizations where spending responsibilities are distributed.

These features signal the next phase of automation, control, and flexibility in business payments.

Conclusion

Business UPI wallets are no longer simple payment tools—they are evolving into full-fledged spend management systems. With instant payments, automated reconciliation, real-time dashboards, ERP integration, and smart spending rules, they offer a level of control and efficiency that traditional methods cannot match.

As businesses continue adopting digital-first financial workflows, the demand for feature-rich UPI wallet platforms will only grow. Solutions like Tera Cloud are already at the forefront of this shift, offering the modern capabilities companies need to eliminate cash, strengthen compliance, and accelerate daily operations.